General accounting

XI. 40. Cash Flow Statement (1): what is cash?

Video

In accounting, there is an apparent contradiction:

- we say that value is the most important concept: that's why double-entry accounting was invented

- and we say that cash is the most important concept: a firm thrives or goes bust depending not on the values in its assets but on the cash it holds.

Double-entry accounting was invented to record a payment received in the form not of money but of a promise (what we've called an "IOU").

This IOU, received in exchange for goods, is not money, but it is value. And as such it is recorded in a "debtors account".

Yet, we pay with cash not with value.

(In this lesson, I assimilate cash to banknotes and coins and money in checking accounts in banks.)

A firm can make profits but go bust because it runs out of cash. Conversely it can make losses and (for a while) have its cash grow.

So what is cash?

The question is difficult and profound. What distinguishes cash from any other value? Why, with few exceptions, can't one pay with value, only with cash?

For a substance to become cash, it must be accepted by everybody as a payment. We are not going to go into the history of money and barter, all the less considering that anthropologists have shown that "barter replaced by money because it is more rational, efficient and convenient" is a fable invented by neoclassical economists in the XIXth century. Money like any other social institution has a religious and sacred origin.

Depending upon societies and epochs, it has been possible to pay with seashells, feathers, hatchets, pepper, cigarettes, nylon stockings, hard-boiled eggs, etc.

A bit of history on precious metals as money, however, will help us understand the simplicity as well as subtlety of cash.

Until the advent of official paper money, in the XIXth century, cash was essentially coins made of precious metals.

A gold coin had 2 values:

- the sign coined on it

- the quantity of gold in it

Over the course of history many monarchs lowered the quantity of gold in coins while keeping the same signs on them.

- It was a way of collecting revenues at times when levying taxes was difficult.

- It was called seigniorage, or even degradation. (I make a long story short...)

- It is also, by the way, an evolution of money toward something equivalent to paper money, that is pure signs on worthless support.

This dual value of coins lead to plenty of problems.

(When two different precious metals, like gold and silver, are used to make coins, the problems created by the four values are even worse, and lead to money making machines.)

Paper money began to appear in the XVIIth and XVIIIth centuries, but only in the XIXth century did each State grant to one of its big banks the monopoly of issuance of official paper money with legal tender status.

In the XVIIth and XVIIIth centuries, too, it began to be understood by people like William Petty (1623-1687) or John Law (1671-1729) that a country to produce and exchange and be prosperous needed money, but that this money didn't have to be made of precious metal. It could be pure signs on slips of paper (= notes).

bankruptcy of the bank of Law, rue Quincampoix, Paris

March to October 1720

When Louis XIV of France died, in 1715, the French Treasury was empty.

Despite the thrifty "mercantilist" policy of Colbert (manufactures...), the four wars fought by Louis and the lavish court expenditures (Versailles...) had dried the Treasury up.

John Law met with the Regent and suggested to set up a bank which would issue paper money (in exchange for gold deposits). It worked for a while: the Treasury was replenished.

After four years, however, distrust and withdrawals (by the Prince of Conti for instance) destroyed the bank of Law.

All along the XIXth century there was a controversy (called "the Bullion controversy") on whether paper money should be guaranteed by gold and to which extend (the currency school), or it didn't matter (the banking school).

In fact, from about 1870 until WWI, during the so-called "Gold Standard Era", all currencies were guaranteed by gold.

An economist said: "A pound sterling, or a dollar, or a franc germinal... were actually only names for certain weights of gold."

After the unstable period of the 1920's and the 1930's, from WWII until 1971 (with some adaptation) currencies were again guaranteed by gold:

- 1 oz of gold was worth $35. (Before WWI it was $20.67)

- all currencies had fixed exchange rates with respect to each other.

Since August 1971, currencies are no longer guaranteed by gold. They represent nothing more than the signs on their banknotes, that is some purely abstract yardsticks. They float with respect to each other.

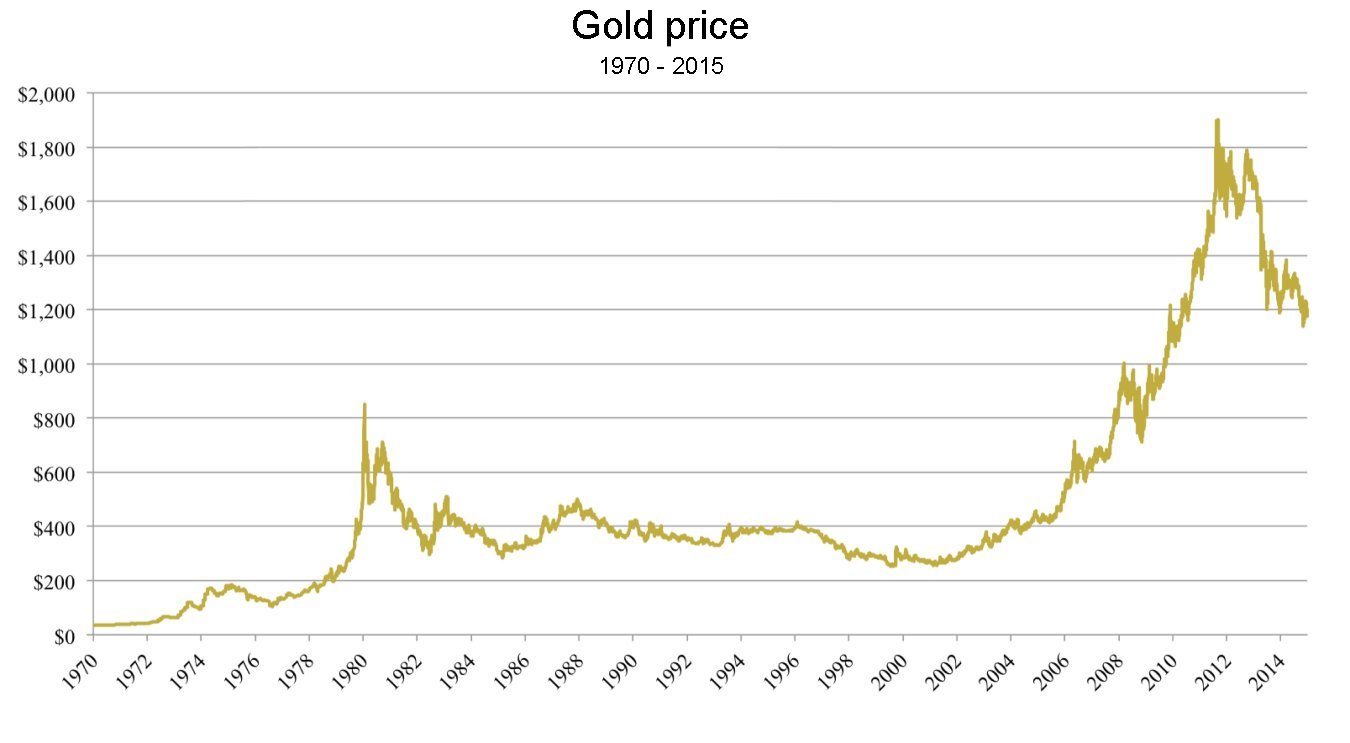

The price of gold began to go through vast fluctuations:

In 2011, it exceeded $1800 per ounce. In May 2016, it is around $1200. (It is the Troy ounce of 31.1035 grammes. It is a cube of gold of edge approximately 1.17 cm.)

One of the main missions of monetary authorities, in each country, all over the world, is to preserve price stability.

That is, a representative basket of goods and services should keep roughly the same value over time.

Indeed inflation is a curse on a community: contracts over time with fixed values become worthless. This destroys the social fabric.

And deflation is almost as dire.

An "obvious" idea, to achieve this goal, is to limit the quantity of official money in circulation.

A supporting argument by some people is to point to the Great Price Revolution of 1500-1650, when prices in Europe were multiplied by 5, and to link it to the huge inflow of precious metals from the New World.

But others retort that this inflation began around 1470, while the metal inflow didn't start before the conquest of the Inca empire by Pizarro, some 60 years later.

"Syndics of the Drapers' Guild", Rembrandt

Rijksmuseum, Amsterdam

The Great Price Revolution corresponds to the transfer of social power from landed aristocracy to merchants (and, in the view of the teacher, was caused by this shift in power), and ultimately lead to the fall of the Ancient Regime.

Monetarism (restriction of the money supply) usually leads only to social hardship: dearth of credit, bankruptcies, unemployment, etc.

At the end of 2010, there are still people advocating going back to currencies guaranteed by gold to sort of limit automatically the money supply. (The teacher does not support such an idea. Many other things will happen to currencies and to nation-States in the XXIst century, but it is another story...)

To conclude:

- it is important for firms to know what explains the evolution of their cash from one year to the next, and to be able to budget it as well.

- it is the objective of the Cash Flow Statement, to explain the cash evolution with big figures from the balance sheets and the income statement, without going back to the detailed journal.

- in the next lesson, we shall see how to construct a Cash Flow Statement.