General accounting

II. 6. Management Information Systems and Accounting

Video

The purpose of the toy manufacturer example is to show that running a firm produces large amounts of information, which the management team must know and monitor in order to run the firm efficiently.

These pieces of information are organised into various Management Information Systems (MIS).

"Management Information System" is the name given to an elaborate database designed to record a certain type of information and make it available through a convenient interface to the management.

A non exhaustive list is:

- monitoring the amount of money at our disposal (present, future)

- general accounting

- productivity measurements

- managing the workforce

- production workforce

- sales team

- administrative staff

- managing the clients (present clients, new clients, prospects, choosing prospects, organising the sales team work)

- managing the production tools (which machines work well, which require maintenance, which should be replaced, why)

- managing the suppliers

- managing the relationship with banks, with the authorities, etc.

- keeping an eye on competition

The accounting system is only one of the various MIS which the management team must have at its disposal, and use to manage efficiently the firm.

There also exists a body of accounting techniques which is called "cost accounting" (or sometimes "managerial accounting"). It extends general accounting into much more details. Its aim is to compute cost and profit per product, and to produce budgets built rationally. It uses data from general accounting as well as from other MIS. We do not study it in this course.

The interested reader can find an introduction to cost accounting in lesson 5 of our course Introduction to finance with a review of accounting, and a more thorough treatment in Courses in business schools and Cost accounting. A prerequisite is a good knowledge of general accounting.

The logbook which we filled with the description of the 18 steps, contains monetary information and non-monetary information.

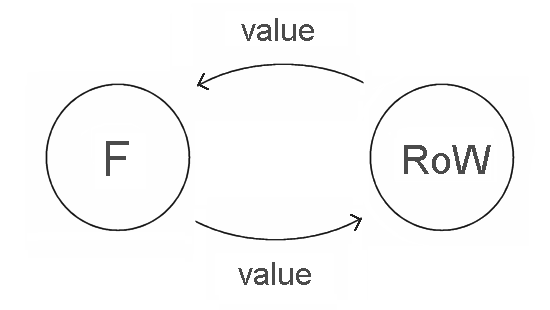

transaction between the firm (F) and the rest of the world (RoW)

Monetary information: The purchase of a van for 4000 € is a monetary piece of information. The sale to Carrefour of 2000 toys in exchange for an IOU is a monetary piece of information, even though no money was exchanged. Both belong to the accounting system.

And both are descriptions of transactions between the firm and the rest of the world. A transaction is an exchange of value between the firm and the rest of the world: value comes in, and value leaves the firm, and the two monetary measurements are equal.

Non monetary information: The observation that we produce 20% wood waste is not a monetary piece of information. It belongs to another MIS. So does the measurement of the number of toys made per day, or the number of calls paid per day, or information about the work contracts with the employees.

The journal is the part of the logbook concerned with monetary information. It is the daily recording of the transactions between the firm and the rest of the world. By definition it belongs to the accounting system. It is its basis.

What is accounting:

Accounting is a set of techniques to record, organise and present in a useful manner monetary information about the activity of the firm. This information, properly organised, and presented in a synthetic way, is very useful to managers. (All relevant information is already contained in the journal, but it is not displayed in a synthetic, useful form.)