Elementary finance

What is a financial product?

Text

introduction

plain vanilla bond

many kinds of financial products

modern money derives from financial products

tangible value

gold

US Treasury bond

US banknote

gold deposit receipt

State powers

slow demise of nation-states

more examples of financial products

Video

A financial product is a contract between two agents stipulating movements of cash now and in the future

We didn't represent an arrow from A to B, because actually there may be no movement of cash today. But there must be movements in the future. They depend on various conditions, stated in the contract.

So, once again, time plays a fundamental role.

The simplest financial product is the "plain vanilla" bond. Let's look for instance at a 1 year 3% bond sold by B to A.

From A's viewpoint, the movements of cash are these

There are many more kinds of financial products:

- insurance policy

- futures

- options

- swaps (exchanging one stream of future payments for another one, possibly in two different currencies)

- complex structured products

- etc.

Modern money also derives from simple financial products. The banknotes we have in our pocket, at first were receipts given by a bank (selected to be a central bank) to a State in exchange for a loan. Let's clarify this sentence which involves several ideas. The operation between the bank and the State goes like this

After the operation the balance sheet of the bank is as follows (suppose it was the first operation of the bank):

The banknotes, initially given to the State Treasury, will be used for the State's expenditures (paying civil servants, various purchases, financing wars...), and will eventually ooze into the population. Without going into details here, the creation of the money we keep in commercial bank accounts follows similar lines.

Many countries selected their central bank in the XIXth century. The Bank of England, created in 1694, became the central bank of England in 1844. The United States are an exception: due to the fierce taste of Americans for independence, they created their own central bank (the Federal Reserve System) only in 1913.

Money will be the topic of our third course in the trilogy: accounting, finance, money

A financial product has value, but it is not tangible. To build our understanding of the various types of values, let's consider several examples.

Tangible value:

sack of rice

This is consumable tangible value. A hammer is also tangible value, but you don't eat it; it is a tool to produce consumable value (for instance, a house in which we will live).

By some sort of convention, since probably neolithic times, gold is considered as "incorporating its own value".

Or, put another way, gold has always been desirable. Because it is rare and pretty, it is suited for display of power and wealth, and furthermore it doesn't alter. So, ever since men are on Earth they have been willing to pay a high value for gold (relative to what wealth produces an hour of work). And this is still the case today.

gold

When President Ben Ali fled Tunisia, after the January 2011 uprisings, he took with him 1.5 tonnes of gold.

$100 US Treasury bond

Second example of receipt/promise:

$100 US banknote

This "receipt" has legal tender status in the United States of America, and various other countries in the world.

Third example of receipt/promise:

receipt of gold deposit at the Banque de France during WWI

We shall study, in our course in money, how come pieces of paper like that can play such an important role in the functionings of a community.

Finance being about promises, it requires powers capable of enforcing them. This is why modern finance and modern money developed in parallel with the emergence, in western Europe, of powerful monarchies, which replaced feudality (having itself come after the collapse of the western Roman empire and the subsequent "barbarian" kingdoms) between 1000 and 1700.

Then absolute monarchies were replaced by various "republican" systems, which retained however (and even reinforced) the centralised authority of monarchies.

At the beginning of the XXIst century, we are witnessing the slow demise of nation-states. This is due to the combination of several factors, among them these two:

- advent of new communication systems which prevent states from controlling the free diffusion of information in their populations

- this is one of the reasons of the ex-Ottoman empire post-colonial state revolutions in Northern Africa

- but this erosion of credibility can also be observed in France

- some new international firms have the capacity to maintain systems of signs (moneys) that are better and more reliable than international State currencies.

Let's leave, for the time being, these momentous topics and return to the description of selected financial products.

Insurance policy. Consider two agents, A (a client) and B (an insurance company). When A subscribes an insurance policy with B, the contract between A and B is this:

- A pays every year a premium to B

- in case of a damage occurring to A, B will pay to A a financial compensation

Futures. At time t (= today), A and B sign a contract stipulating a price and a date T (in the future) at which they will exchange goods for money. Futures contracts are usually binding.

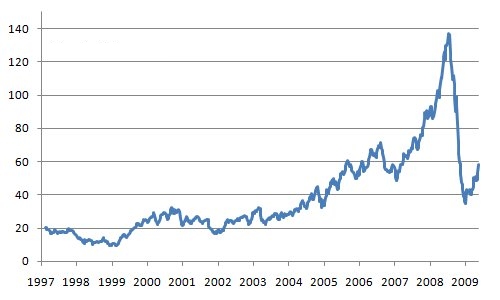

For instance, when the price of oil reached $140 in 2008, Air France found "futures" investors willing to sell it kerozen at some future dates at $200 per barrel. Air France entered into large such contracts. They were intended to cover the company against possibly even higher prices in the future. Unfortunately, prices subsequently plummeted, and for a while Air France paid its kerozen very dearly.

oil price 1997-2009 ($/barrel)

Futures have existed at least since Thales of Miletus (624 bc, 546 bc) about whom there is an anecdote according to which he astutely entered into some futures contracts on olive oil processing in order to prove to some critics that philosophers could also be practical.

Today (February 15th, 2011) Google stocks trade for $628.

Here is an example of option:

- A and B agree today that B will be willing to sell to A one Google stock for $600, on June 11th, 2011

- A pays today to B $50.8 for this right

Such an option is called a "call option".

Then, on June 11th, if the price of Google stocks is higher than $600 A, will "exercise" its option, and buy one stock from B (and usually resell it right away, pocketing the difference between the market price and his exercise price). If on June 11th, on the other hand, the price of Google stocks is lower than $600, A won't exercise its right and simply discard his option.

Screens of the video

|

|

|

screen number display zone |

Course table of contents

Contact