Esc-Clermont Sup de Co

2nd

years, 1st semester

Course:

Corporate finance

Teacher:

André Cabannes

Please write your

name in this box:

Final exam

December, 2005

3 hours, 20 questions, each worth 5 points.

Write your answers on this document in the blank space below each question.

Question

1: The firm F sells

computers. The firm G sells flowers. F sells a computer to G for 2000€, on

credit. Let’s look at this transaction from F point of view: what are the two

entries made for this transaction in F accounting system ?

Credit

the sales account 2000€

Debit

the debtors account 2000€

Now, let’s

look at this transaction from G point of view: what are the two entries made in

G accounting system ?

Credit

the suppliers account 2000€

Debit

the fixed assets (computers) account 2000€

Question

2: Is the asset

side of the balance sheet of a firm the list of all the values today of what the firm owns? (Hint: Make

comments on the Historical costs rule.)

No.

The asset side of the balance sheet of a firm lists all the assets the firm

owns, recorded at the historical cost. Typically, land acquired a long ago is

usually undervalued.

Question

3: Why the credit

and debit columns of a trial balance should add up to the same number?

Because, each transaction leads to an entry on the

debit side of an account, and to another entry with the same value on the

credit side of another account. So, globally, along the year, the debit entries

and credit entries remain always equal, and so are their balances.

If they add

up to the same number, does this prove that the trial balance is necessarily correct ?

No.

There are mistakes which do not create imbalances ;

for instance, to reverse a debit entry and a credit entry.

Question

4: A firm sells for 120€, cash, an item recorded

at 90€ in its stocks : show the impact of this

operation on the balance sheet.

The

stocks account will decrease by 90€. The cash account will increase by 120€.

And, on the liability side, the profit account will increase by 30€.

Can a firm

sell something at a lower price than its purchasing cost ?

(Discuss.)

Yes.

It will result in a loss, for this operation. (In some economic sectors, it is,

in theory, forbidden.)

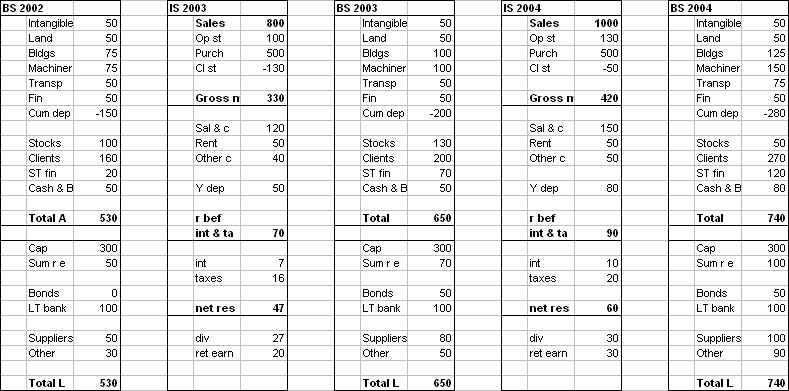

Consider

the following year end documents of a firm. Questions 5 to 8 refer to these

data.

Question

5: What are the Net

Fixed Assets at the end of 2002, 2003, and 2004 ?

End

of 2002: 200

End

of 2003: 200

End

of 2004: 220

Assuming

that the firm did not sell or otherwise remove any fixed assets from its

balance sheets, what were the investments in fixed assets in 2003 and 2004?

2003:

50

2004:

100

Question

6: What is the ROCE

ratio in 2003 and in 2004?

ROCE = result before interest

charges and taxes / capital employed (or averaged capital employed)

Using

simply end of year capital employed,

ROCE

2003 = 70 / 520 = 13,5%

ROCE

2004 = 90 / 550 = 16,4%

Question

7: What do we mean

by “this firm doesn’t use much its free financing possibilities” ?

The

free financing of a firm is (approximately) represented by its current

liabilities, i.e. those liabilities which do not cost anything in terms of

financial charges. In the example above, the current liabilities are much lower

that the current assets. The liquidity ratios of the firm are very high.

Presumably, the firm could obtain more credit from its suppliers and other

“free” creditors.

Question

8: Prepare the Cash

Flow statement of the firm for the year 2004.

Cash flow in: 930

Sales

= 1000

Minus

increase in debtors = – 70

Cash flow out: 900

Purchases

= 500

Cash

operating expenses = 250

LT

Investments = 100

Taxes

& Dividends = 50

Minus

increase in suppliers and other creditors = – 60

Interest

charges = 10

Increase

in short term securities = 50

So,

the net variation in cash is + 30.

Question

9: What

distinguishes General Accounting and Cost Accounting ?

General accounting (IS & BS)

•

Gives a very general view of the firm

•

Legally required, and the year end docs must be published

•

Turned toward the

past

•

Too global to be useful to manage the firm

•

Comes late

Cost

accounting (Sales per product lines and costs in every « cost centers)

•

Useful to manage the firm

•

Turned toward the

future

•

Very detailed

•

More or less in real time

What is a

cost center? What is a profit center?

A

cost center is any small subdivision (physical or

logical) of the firm where costs are generated.

A

profit center is a subdivision of the firm to which

we can associate not only costs but also sales, and therefore a (partial or

complete) income statement.

Question

10: Why complete

unit costs are artificial ?

Because

they require “allocation keys”, to allocate fixed costs, to be computed, and

they depend upon all the activities of the firm.

For

instance, a workshop manufacturing 10 000 chairs per year, will have a

complete unit cost per chair that depends on whether it also makes other pieces

of furniture.

Question

11: Consider a

security S which can be purchased today. In one year, it will have a value X

which is random (depending upon the state of the economy). The possible values

of X, with their respective probabilities, are given in the following table :

|

Possible outcomes |

80 € |

90 € |

100 € |

110 € |

120 € |

130 € |

|

Probabilities |

10% |

15% |

25% |

25% |

15% |

10% |

If a money

management fund purchases S today, for a price P, how will it record this transaction

in its accounting system? (Debit and Credit.)

It

will credit its cash or bank account with a value P. And it will debit a

financial assets account with the same value P.

Question

12: What is the expected

value of S in one year? (Explain your calculations.)

E(X)

= 105€

It

is the weighted average of the possible outcomes of X.

What is the

standard deviation of the value of S in one year? (Explain your calculations.)

Std

dev (X) = 14,3€

It

is the square root of the variance of X. And the variance of X is the weighted

average of the possible squared deviations of X around its mean.

Question

13: In the euro

zone, in November 2005, what was the rate of return of a risk free security?

2%

What is the

price today (at the date of preparation of this exam, in mid-November 2005) of

a risk free security that will be worth 105€ in one year ?

105€

/ 1,02 =

102,94€

Is S (of

question 11) risk free?

No.

Its value next year has variability.

Question

14: Suppose S sells

today for a price P = 92€. What is the expected profitability of S?

rS = (105 – 92) / 92 =

14,1%

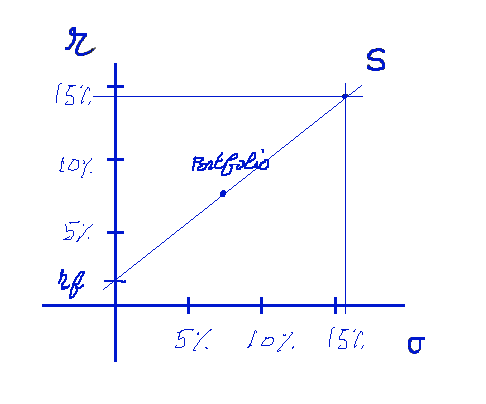

Position S

on the risk return graph?

We

must compute the risk of S, defined as the std dev of its profitability

: it is 15,6%

Question

15: Suppose we have

920€ to invest. We want to invest this sum into a “portfolio” constructed as follows : half of our money is invested into safe treasury

bills and half into S. What is the expected value of our portfolio in one year ?

Answer:

469,2€ + 524,9€ = 994,1€

Position

our portfolio on the risk return graph.

Question

16: Explain the

concept of present value. Use the following example :

why a sum of 100€ promised in one year is not worth 100€ today ? What happens

to its present value if its future value is risky?

A

promise for 100€ in one year is not cash today. Therefore we cannot use it as

cash to make an investment, and earn money with our investment. Therefore, if

we buy this promise today, we “give up” the possibility to have our own money

work. So, we should buy this promise for less than 100€.

If

the promise is risky, its price today is even less than if it is not risky.

The

present value of a future cash flow is the maximum cash amount that we would be

willing to pay today, to acquire the promise to receive the cash flow in the

future.

Question

17: We are

considering making an investment I, which will produce the following cash flows

in the future for us :

|

(mio euros) |

year 0 |

year 1 |

year 2 |

year 3 |

year 4 |

|

|

|

|

|

|

|

|

Future

cash flows |

|

50 |

100 |

130 |

80 |

Suppose

this investment has the same risk pattern as S above, i.e. its opportunity cost

of capital is r = 14,1%. What is the Present value of

the stream of future cash flows of I? (Show your

calculations.)

Answer:

255,35 mio euros.

|

Discount

rate |

14,1% |

|

|

|

|

|

|

|

|

|

|

|

|

(mio euros) |

year 0 |

year 1 |

year 2 |

year 3 |

year 4 |

|

Future

cash flows |

|

50 |

100 |

130 |

80 |

|

PV of future cash flows |

|

43,82 |

76,81 |

87,52 |

47,20 |

|

Sum of PV |

255,35 |

|

|

|

|

If we can

make this investment with an initial cash-flow-out of 200 millions euros to be

spent year 0, is it a good investment?

Yes,

because 200 is less than 255,35, and therefore the Net

Present Value of the investment is positive.

Question

18: Explain what we

mean by the IRR of an investment.

If

the initial cash flow to be invested (here 200 mio

euros) is already known, it is the value of the discount rate which makes the

NPV equal to zero.

Suppose we

can make I with CF year 0 = 200 mio

euros. What is the NPV of I, if the proper discount

rate (i.e. the opportunity cost of capital) is 20%?

224,9 mio euros – 200 mio euros = 24,9 mio.

What is the

NPV if r = 30% ?

184,8 mio euros – 200 mio euros

Estimate

the IRR of I.

A

geometric interpolation yields around 26%.

Question

19: What is one of

the central ideas introduced by Finance which distinguishes it from Accounting?

The

present value of future money is less than its face value.

Question

20: Suppose we want

to buy 100% of a firm, which already exists and already has a few past income

statements and balance sheets, from its shareholders. Why the “value of the

firm” to the shareholders (and therefore the minimum price we will have to pay

them) may be more than the total equity shown in the balance sheet (total

assets minus liabilities to external agents)?

For

the owners of the firm, i.e. the people owning its shares of capital, the value

of these shares is the money they will generate for them in the future,

properly discounted. It is not directly related to the balance sheet, which

records the value of the assets and liabilities of the firm today.