Esc-Clermont Sup de Co

2nd

years, 1st semester

Course:

Corporate finance

Teacher:

André Cabannes

Write your name in

this box:

Final exam

December, 2008

20 questions, each worth 5 points. Write your answers on this document in the blank space below each

question.

Question

1: Your firm has,

in its balance sheet, some fixed asset the net value of which is 100 (raw value

600 and cumulated depreciation 500). You sell this asset for 150 in cash.

Explain the impact of this transaction on the asset side and the liability side

of you balance sheet.

FA decrease by 100

Cash increases by 150

Total assets increase by 50

Retained profit increases by 50

Total liabilities increase by 50

Question

2: At the beginning

of the year, the inventories were 230. During the year, the purchases were 550.

And at the end of the year, the inventories were 180. What was the cost of

goods sold?

600

Question

3: Explain what is a “non cash yearly expenditure”. Why are they important to

get an accurate view of the result of the year?

It

is a decrease, during the accounting period, of the

value of some of the assets of the firm. Typically it is the “wearing out” of

Fixed Assets. It can also be provisions for bad client paper. It does not

correspond to any cash outlay, but it must be recorded in the IS as an

expenditure. It is a non cash expenditure.

Remember

that double-entry accounting is a “value accounting” system, as opposed to

single-entry accounting which is only concerned with cash.

Question

4: The ROCE is defined

as

[net result + interest

charges + income taxes] / [average capital employed]

while the

ROE is defined as

[net result] /

[average net worth]

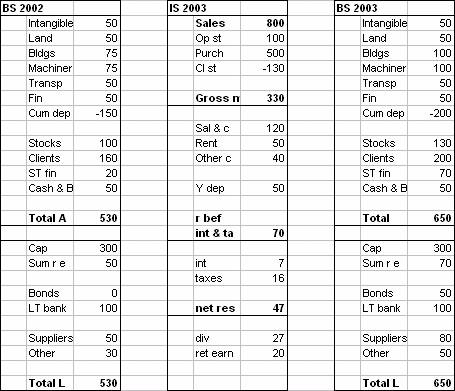

Consider

the following year end documents

What is the

ROCE? And what is the ROE?

ROCE

= 70 / [ ( 520 + 450 ) / 2 ] = 14,4%

ROE = 47 / [ ( 370 +

350 ) / 2 ] = 13,1%

Question

5: Explain what we

mean by “the ROCE measures the performance of the firm, disregarding its

capital structure”.

The

ROCE looks at the value generated from operations (before interest and taxes)

by the capital employed.

Whether

the structure of the capital employed is made of much capital and little debt,

or on the contrary of much debt and little capital (i.e. a

high debt leverage), does not change the total capital employed. And on

the numerator side, the result before interest and taxes is not affected by the

structure of the capital employed either, because only financial charges and

therefore taxes change.

So

the ROCE is indeed a measure of the value generation capacity of the capital

employed disregarding how they are constructed.

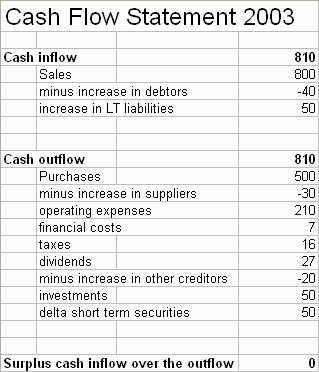

Question

6: Establish the

cash flow statement of the firm the year documents of which are given above in

question 4.

See

course notes lesson 4a

Question 7: You have in your pocket today (date

t) a security promising to pay you a certain sum X in the future at date T,

signed by the issuer. What are the three factors affecting the value of this

security today?

The

face value X (the sum written on the security)

The

length of time (T – t)

The

creditworthiness of the issuer (i.e. the risk that he does not pay you)

Question

8: What are the

main concepts added by Finance onto Accounting?

The

role of time, and the role of risk.

Why does

the Modern Theory of Finance make use of probability theory?

There

are circumstances when the future payments we expect are not sure figures but

figures which may vary. We then use the modelling framework of probability

theory to represent this variable situation: the future sum we shall receive will

be the outcome of a random variable in the experiment “wait until payment”.

Question

9: We can buy

today, in the stock market, a security S for a price PS = 35 euros.

We know, from a study of the past behaviour of S, that its value in one year

will be a random value X, with the following characteristics:

|

Possible future value (in euros) |

25 |

30 |

35 |

40 |

45 |

50 |

55 |

|

|

|

|

|

|

|

|

|

|

Probability |

5% |

10% |

15% |

40% |

15% |

10% |

5% |

What is the

expected value of X? (show your calculations)

Compute

the weighted average of the possible values with their probabilities as

weights.

(25

x 5% )+ (30 x 10%) + … + (55 x 5%) =

40 euros

You

may also notice that the calculations being “symmetrical around 40” (in the

sense that the same weights are put on pairs of figures, each pair averaging

40), this central figure of 40 must be the result, because all the weights add

up to 1.

Question

10: What is the

expected profitability of S?

The

profitability of S is defined as RS = (X – P) / P

RS

is a random variable.

E(RS) = (40 – 35) / 35 = 14,3%

Question

11: What is the

standard deviation of X? And what is the risk of S?

The

standard deviation of a random variable is the expected value of the squared

deviation of the random variable around its mean.

Standard

deviation of X = sX = 7,07 euros

The

risk of S is defined as the standard deviation of RS

It

is 7,07 / 35 = 20,2%

Question

12: There is

available in the stock market a security T for a price PT. The value

of T in one year will be a random value Y, with the following characteristics:

|

Possible future value |

75 |

90 |

105 |

120 |

135 |

150 |

165 |

|

|

|

|

|

|

|

|

|

|

Probability |

2% |

6% |

18% |

48% |

18% |

6% |

2% |

Is T more

or less risky than S?

We

compute E(Y) and sY.

E(Y)

= 120 euros

sY = 16,43 euros

Then

we observe that Y is relatively less variable around it mean than is X

sY / E(Y) = 0,137 while

sX / E(X) = 0,177

so T is less risky than S.

What can we

already say about the price of T?

Since

T is less risky than S, T will have less profitability than S.

The

profitability of S is (40 – 35)/35, which is also (120 – 105)/105.

So

T has to be worth more than 105 euros on a rational market with no arbitrage

possibilities.

Question

13: We are

considering making the following physical investment in our firm

|

year |

0 |

1 |

2 |

3 |

|

|

|

|

|

|

|

CF

(millions of euros) |

-80 |

40 |

40 |

40 |

What are

the two fundamental rates attached to this investment?

The

opportunity cost of capital

The

IRR

Question

14: Suppose that this investment belongs to the same class of risk as the

security S of question 9 above. Is this investment worth making? (show your calculations)

If

this investment belongs to the same class of risk as the security S, then its

opportunity cost of capital is the expected profitability of S, that is 14,286%

(if we want to be – overly – precise).

Then

the PV of the first cash flow in one year is 35 million euros.

The

PV of the second cash flow in two years is 30,63

million euros.

And

the PV of the third cash flow in three years is 26,80 millon euros.

In

other words, the three cash flows we expect to receive are worth today 92,42 million euros.

If

we can create this project for 80 million euros, it is a good deal.

Question

15: What is the IRR

of the investment of question 13?

We

know that the IRR must be more than 14,3%

We

try calculations with 20%, and we still a positive NPV of 4,3

million euros.

The

we try a discounting rate of 25%, and we get NPV = -1,92

million euros.

Then

we may do a linear interpolation between 20% and 25%,

x satisfies the equation

x / 4,3 = ( 5 –

x ) / 1,92

this yields x = 3,46

and therefore an approximate IRR of 23,46%

The

exact result is 23,37%

Question

16: We have a big

firm making some widgets. We are considering buying 100% of another firm, which

will help us produce more widgets more efficiently.

Why the standalone cash flows of the projected acquisition are not what is

important to us in evaluating the price we should be willing to pay?

If

we buy the entire firm and it will help us produce widget more efficiently, the

new firm will change (for the better) our cash flows,

independently of the standalone cash flows of the new firm.

It

is like the key to a treasure trunk (like Skype was

for eBay). Then the standalone cash flows of the new firm are irrelevant. What

matters is what extra cash flows it will release for us.

Question

17: We buy today

for $1000 a 5year 6% bond (of the most basic type, paying yearly coupons). What

is the series of cash flows we are expecting in the future?

|

year |

1 |

2 |

3 |

4 |

5 |

|

|

|

|

|

|

|

|

cash flow |

60 |

60 |

60 |

60 |

1060 |

Question

18: Two years have

passed (and we have pocketed two coupon payments), and now we want to sell this

bond. The current rate for 3year bonds with the same ratings is 4%. What is the

value of our bond in the secondary market?

|

new discount rate |

|

|

|

|

|

4% |

0 |

1 |

2 |

3 |

|

|

|

|

|

|

|

cash flows |

|

60 |

60 |

1060 |

|

|

|

|

|

|

|

yearly PV |

|

57,6923 |

55,4734 |

942,336 |

|

|

|

|

|

|

|

total PV |

1055,501821 |

|

|

|

Our

second hand bond is worth 1055,5 dollars.

Question

19: What is a junk

bond?

It

is a bond with a very high risk of failure of the issuer, but also a very high

expected profitability (even taking into account the risk of the issuer).

Question

20: Suggest another

way than probability theory to assign present values to promises of future

payments. (Any suggestion will be worth a few points. Thoughtful suggestions

will be worth 5 points.)