General accounting

II. 8. Main concepts of accounting

Video

Even though the toy manufacturer example is rather simple and commonsense, almost all the main concepts of accounting are already there.

Initial capital: it is also called the founding capital. In our example, it was 50 000€ gathered at first in order to pay for the various expenditures we shall have before cash begins to flow into the firm from its operations.

Assets: at any point in time, we can list the things that the firm owns. We did this just after the sale of toys to a first client (list of assets).

retail bank

Relationships with banks: in our example, the bank has a simple role: it manages the checking account of the firm. Banks do of course other things.

Types of banks: there are two types of banks

- Retail banks

(also called "commercial banks")

- manage checking accounts of firms and of individuals like you and me

- manage saving accounts

- receive deposits

- lend money

- Investment banks

- help large corporations with merging & acquisition (M&A) operations

- help large corporations with the issuance and selling of bonds to borrow large sums of money, not from banks but directly from financial markets

Banks which carry out both activities are called universal banks.

It is a big debate, all over the world, to decide whether banks should be allowed to carry out both activities, or the two activities should be done by independent outfits (see the history of the Glass-Steagall act in the United States).

Capital expenditures: these are expenditures for things which will stay in the firm and be used for several years. In our example: the van, the mechanical saw, the computer, etc.

Current expenditures: expenditures for things which will be consumed quickly: work, raw materials, electricity, rent (or more precisely, the right to occupy premises), etc.

Stocks: they are also called inventories. We saw inventories of raw materials, and inventories of finished goods waiting to be sold. When we listed the assets of the toy mfr there were no more raw materials, and there were 1000 toys ready for sale.

Employees: they are the people who sell work to the firm under a work contract.

Client paper: also called debtor paper, IOU, bill, draft, etc.

- It is a most important concept

- It is value but not money

- It is the search for the proper way to record IOU's which triggered the invention of double-entry accounting in the XIIIth and XIVth centuries in Northern Italy

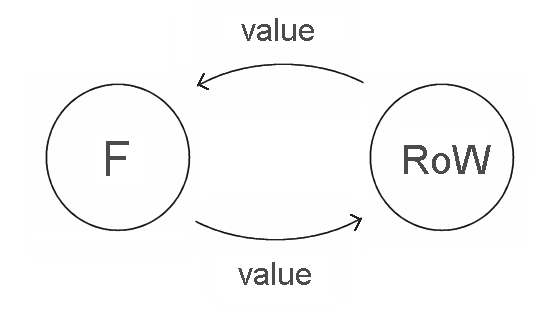

Transaction: finally we cannot stress too much the concept of transaction. It is the elementary piece of activity of the firm. It is an exchange between the firm and the rest of the world.

Value comes in and value leaves the firm. Both values are recorded with the same monetary measurement, and they are recorded as having happened at the same time.

For instance when we sell goods on credit to Carrefour, at the time of the sale goods leave the firm, and an IOU enters the firm. Later on, another transaction takes place: Carrefour pays us, and the IOU has no longer any value.

Examples of transactions:

- purchase of a van (without credit):

- in: a van comes in

- out: cash (or the equivalent in our bank account) leaves

- buying of work:

- in: every month we have received work from our employees

- out: we pay salaries

- paying rent:

- in: we receive the right to occupy the premises for a given period

- out: we pay the rent

Transactions always have two legs (a mouvement in, and a mouvement out). It is when we overlook this fact – to which there is no exception – that confusion sets in.

General accounting is the organised process of recording transactions.