General accounting

I. 1. What is a firm?

This lesson and the next seven are introductory. If you want to enter directly into the heart of double-entry accounting, please go to lesson 9: Why single-entry accounting, like in our checkbook, is insufficient.

Video

Wealth is created all over the world either by individuals and small groups for their own consumption, or by firms to exchange on markets. In this course we are concerned with firms exchanging on markets.

We shall describe the most typical firms, keeping in mind that there exists a wide variety of types (including firms comprising only one individual, or even none).

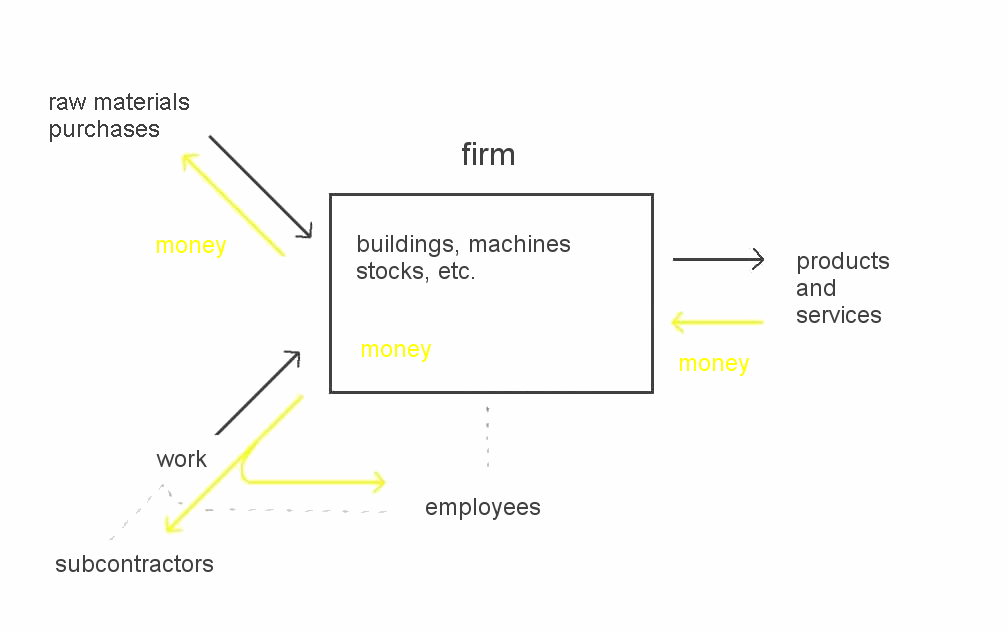

A firm is a group of people, with production tools, located in some premises, who, with work, transform raw materials into goods and services, and sell them.

The work and the raw materials are bought on some markets, and the goods and services are sold on other markets.

Physical and monetary flows: The flows of physical things (including work) are shown below in black, and the monetary contraflows of money in yellow. We shall see that the latter can be money (as shown in the picture) or promises to pay later.

In the rectangle are listed the main assets of the firm.

Types of firms: We distinguish three types of firms:

- industrial firms: think of a workshop, a plant, or a group of plants (in this crude typology into three categories, in "industrial firms" we include farming, mining, transportation, any production of products or services... except selling and finance)

- commercial firms: think of a retailer, a wholesaler, or a large commercial organisation

- financial firms: banks, insurance companies, mutual funds

In the three cases, the accounting techniques which we shall study are identical.

Legal structures: In modern societies, a firm has the legal status of a moral person. It can sign contracts, hire employees, borrow money, get credit, buy and sell goods and services.

The two most common legal structures are:

- the small limited liability firm (or even in some places the sole proprietorship, where the owner is liable of any debt of his firm on his own wealth)

- the joint stock corporation (which also has a limited liability) listed on a stockmarket

The limited liability feature means that in case the firm incurs big losses and is unable to pay amounts due, the responsibility of its owners is limited to the initial money they put in. More explicitly, this means that the owners may lose their initial investment: their shares in the firm may become worthless. But they are not required or obliged to pour more money into the firm to make up for the losses. In case of bankruptcy the irrecoverable losses are born by the various entities to which value was due (suppliers, State, lenders, etc.). This legal structure was introduced in the XIXth century, and is said to have spurred the economic development of the West.

A firm has owners, also called shareholders. The firm owns various things, called assets: buildings, machines, inventories, other things we shall see. And it has a reserve of money, some of it on the premises, most of it "in a bank", that is, managed by a bank (see note).

The firm has employees. These are men and women from whom the firm buys work under a hiring contract. The firm can also buy work from outside subcontractors.

Activities: Commercial firms buy and sell goods without performing any physical transformation on them. Their activity is made of all or part of selecting, transporting, warehousing, distributing, displaying these goods, helping clients, etc.

Industrial firms transform the raw materials and other supplies they buy into finished products which they generally sell to commercial firms. A firm which combines industrial and commercial activities (or more generally combines several big steps of value added) is said to be "vertically integrated".

The main activity of banks is to receive deposits from savers, and to lend this money to borrowers for investment projects or, since WWII, for consumption prior to payment.

All these comments are very general. Their purpose is only to set a framework before going into the study of accounting.

What is accounting about? : One of the objectives of accounting is to determine, over a period of time (for example a calendar year), what profit or what loss the firm incurred.

In short, if the sales value of the products and services which the firm sold exceeds the complete cost of production of these products and services, the firm will register a profit. Otherwise, it will register a loss.

To compute the sales value of all the products and services sold is not complicated. On the other hand, to compute the complete production cost (without omitting anything, nor counting too much expenditures) requires a bit of care.

To this end, we will introduce accounts of various nature. Each operation of the firm will give rise to two recordings (one in one account and another in another account -- hence the term "double entry accounting" --, we will see all this in detail starting lesson 9).

We will also produce some sort of state of the firm at any date. It is the document called the "balance sheet". This document will list everything that the firm owns, as well as everything that it owes to creditors, or to its shareholders. There again, this sentence will become clear once we have completed the course.

Accounting provides tools and dashboards which are very important to manage the firm (see last section of this lesson).

A bit of history: Commercial firms and banks, as we know them, date from the late Middle Ages, at the time of strong development (demographic, economic, cultural) which Western Europe experienced between 1100 and 1300 even before the Renaissance.

Whereas if you except shipyards and some XVIIth century "manufactures", industrial firms date only from the Industrial Revolution, which began in England in the mining and textile industries in the second half of the XVIIIth century, following social changes and the invention of the steam engine.

Protectionist laws passed in the middle of the XVIIIth century to protect the English woolen industry from Indian cotton imports played a role too: when only raw cotton was allowed to enter, English engineers created the flying shuttle, the spinning Jenny and other machines to produce cotton cloth locally.

These technical innovations, together with the steam engine and railways, spurred industrial development and within a few decades the onset of the modern wold.

Management information systems: So a firm is an organisation, with a managerial team. This team needs a great deal of information, internal and external, in order to correctly manage the firm. The elements of information are organised into various "management information systems" (MIS) for the use of the managers and sometimes partners of the firm.

General accounting is one of these MIS. It is the subject of this course.

Note: We write "in a bank" between quotes, because the notion of where is money or a promise is not as simple as ordinary intuition suggests. If you promised your friend John to pay him 80€ in a fortnight, where is your promise? This innocent looking question is at the crux of much confusion about money and currencies. Another example of erroneous intuition: if you see someone burning a banknote, it is certainly shocking, but he or she is not really destroying value; in fact that person is just giving money to the State!